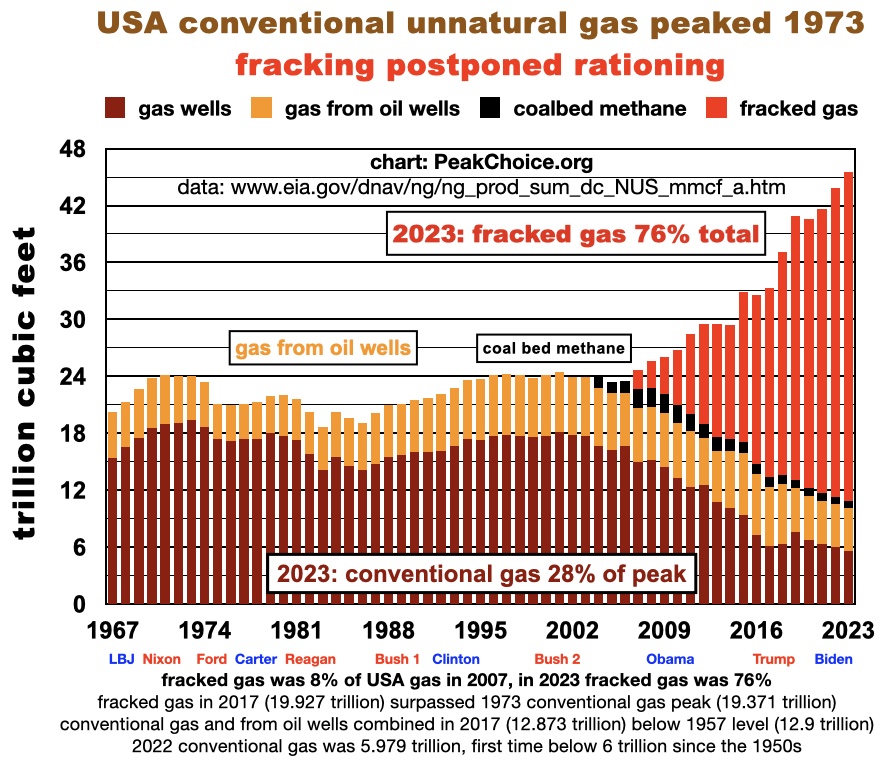

Fracking Postponed Rationing

What the Frack? scraping the bottom of the barrel is not good to the last drop

Grabbing it all as fast as they can: Obama-Biden began boom, Trump made fracking huge

related pages: experts warn about fracking & depletion - Tar Sands: two-thirds of Canada's oil from tar sands

a toxic gas bubble

a toxic gas bubble

- Fracking is a short term, toxic, expensive, desperate effort to offset declining conventional oil and natural gas supplies.

- Fracked oil pushed domestic oil above the peak of conventional oil in 1970. The US is still a net oil importer.

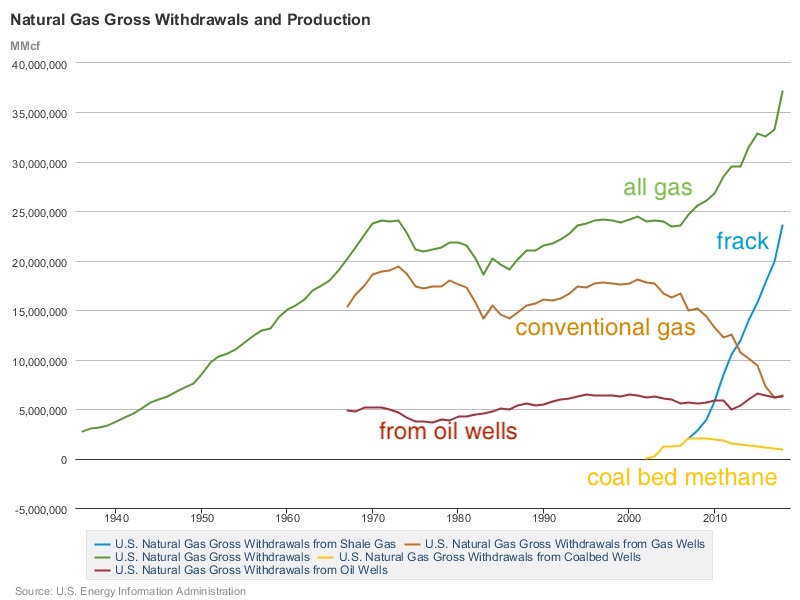

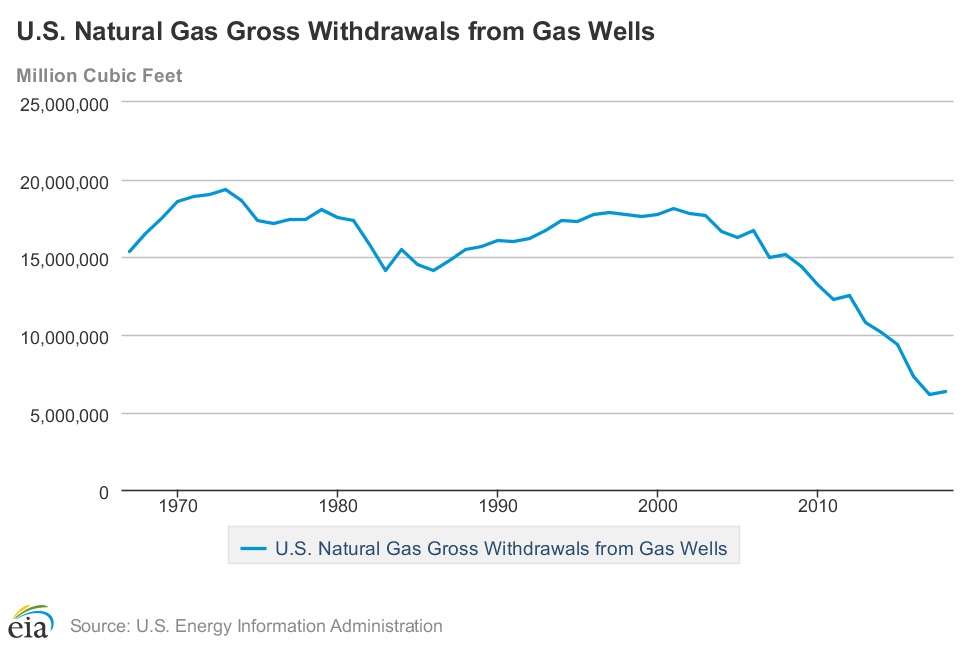

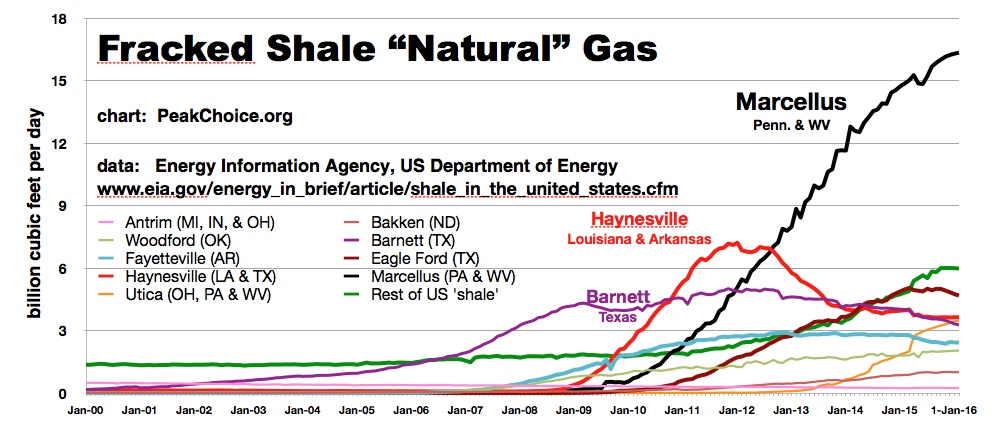

- Fracked gas is now a greater flow than the peak of conventional unnatural gas in 1973.

- fracking cannot provide "100 years" of natural gas for the US, even if environmental and public health concerns are ignored. Fracked wells deplete faster than conventional wells and take more technical expertise, money and energy to drill.

President Obama and Vice President Biden presided over the start of large scale fracking for oil and gas, due to continued declines of conventional oil and gas. The fracking boom boosted the actual, physical economy in the wake of the economic shocks of 2008. The Trump administration accelerated fracking which has further sustained and inflated the economic bubble, obscuring drops in conventional fuels.

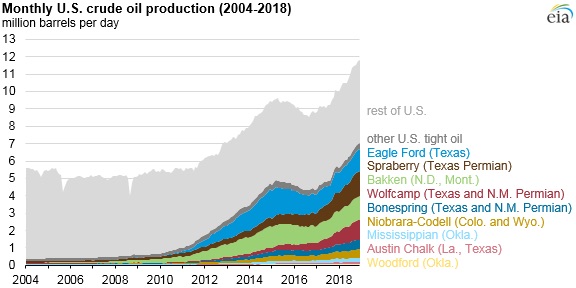

President Obama and Vice President Biden presided over the start of large scale fracking for oil and gas, due to continued declines of conventional oil and gas. The fracking boom boosted the actual, physical economy in the wake of the economic shocks of 2008. The Trump administration accelerated fracking which has further sustained and inflated the economic bubble, obscuring drops in conventional fuels.- The earliest fracked fields have mostly peaked and declined. Fracking fields where production has declined - Barnett (gas) near Fort Worth, Texas and Haynesville, Louisiana - dropped due to geologic constraints, not climate protests.

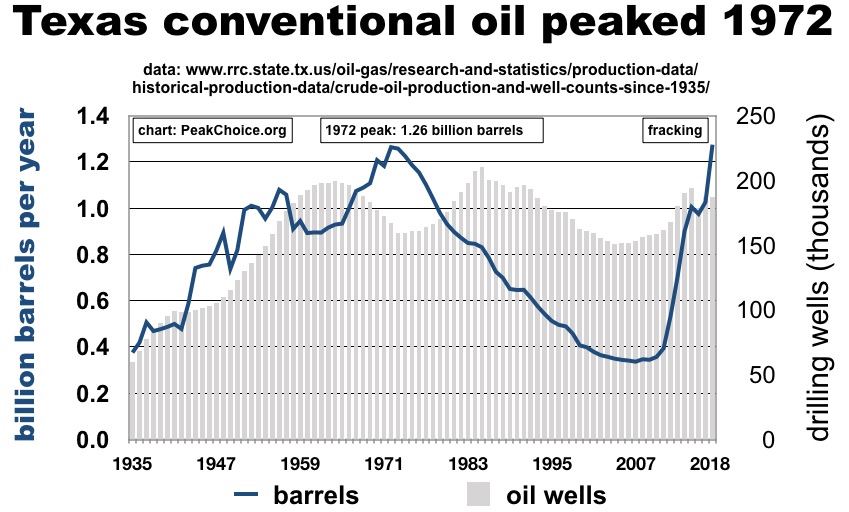

- For oil, the end game for fracking is the Permian in West Texas and New Mexico - ironically next to proposed national nuclear waste dumps.

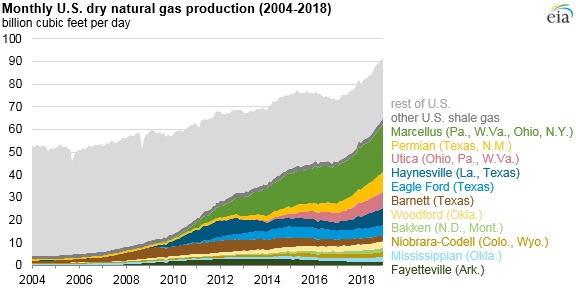

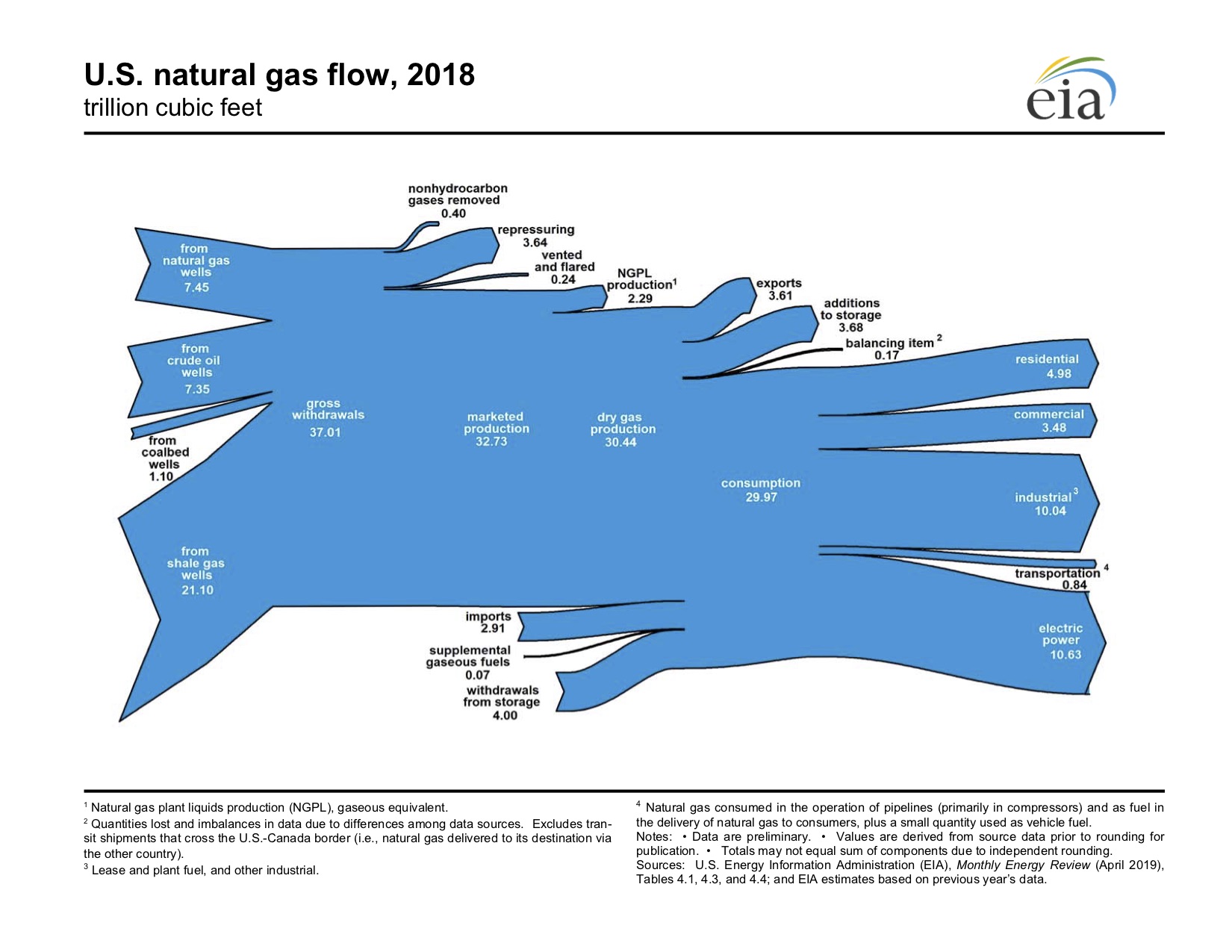

The motherlode of shale gas continues to be the Marcellus in the central Appalachians, primarily Pennsylvania but also neighboring states of Ohio, West Virginia and New York. New York State has banned gas fracking but continues to import fracked gas from Pennsylvania in part to heat their cities in the winter.

The motherlode of shale gas continues to be the Marcellus in the central Appalachians, primarily Pennsylvania but also neighboring states of Ohio, West Virginia and New York. New York State has banned gas fracking but continues to import fracked gas from Pennsylvania in part to heat their cities in the winter.- Senators Bernie Sanders and Elizabeth Warren promise they would ban fracking if elected, echoing demands from environment and climate movements. However, the consequence for banning fracking would be an immediate reduction of burning natural gas for electricity and heating cold cities, plus the start of gasoline rationing. This is why environmental objections to fracking have been unsuccessful.

www.eia.gov/todayinenergy/detail.php?id=38372

FEBRUARY 15, 2019

EIA adds new play production data to shale gas and tight oil reports

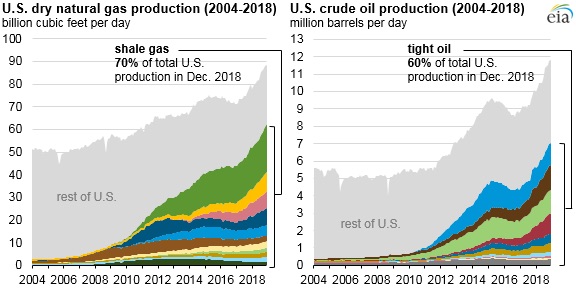

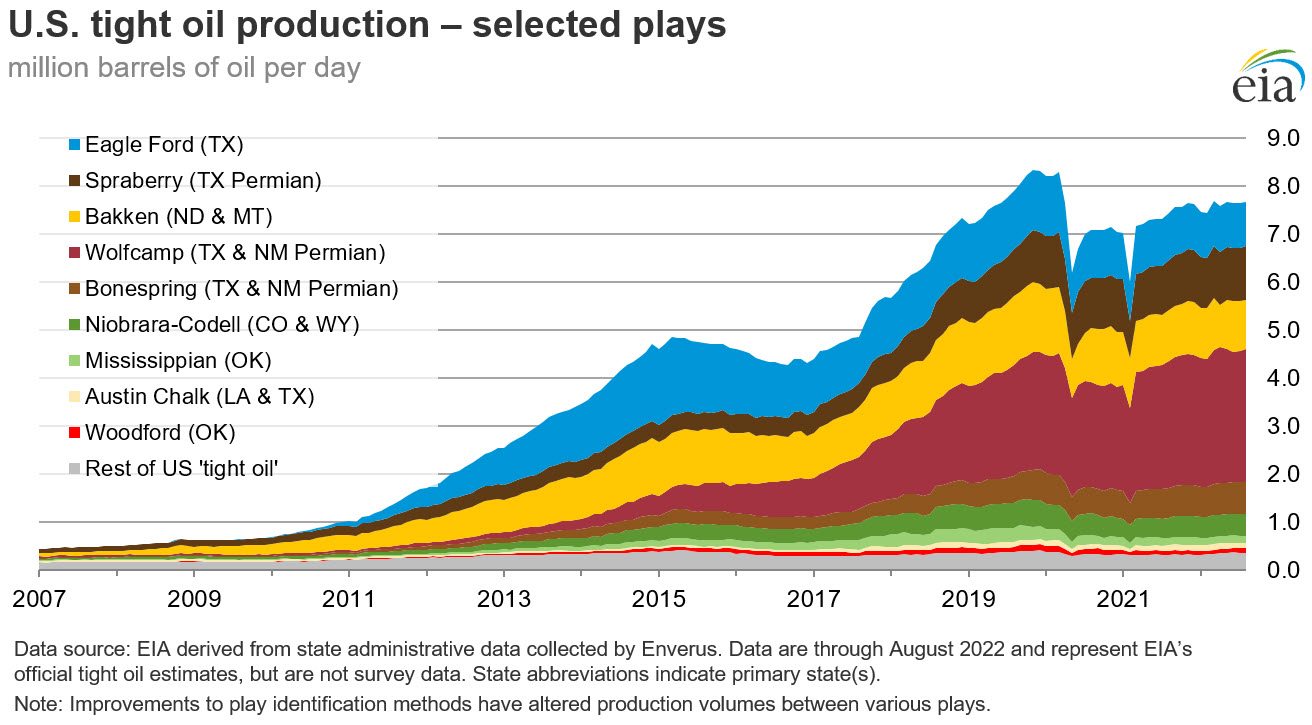

"In December 2018, U.S. shale and tight plays produced about 65 billion cubic feet per day (Bcf/d) of natural gas (70% of total U.S. dry gas production) and about 7 million barrels per day (b/d) of crude oil (60% of total U.S. oil production). A decade ago, in December 2008, shale gas and tight oil accounted for 16% of total U.S. gas production and about 12% of U.S. total crude oil production."

in these graphs, the gray zone is the conventional oil and natural gas production. Note that the ongoing energy boom is entirely due to fracking. Conventional, non-fracked fuels are in sharp decline.

Conventional nat. gas peaked in 1973 at over 50 billion cubic feet per day.

Conventional oil peaked in 1970 at about 10 million barrels a day.

How long fracked wells obscure the decline of conventional wells determines much about the future of the "economy" in the USA in the 2020s.

From Obama to Trump: grabbing it all as fast as they can

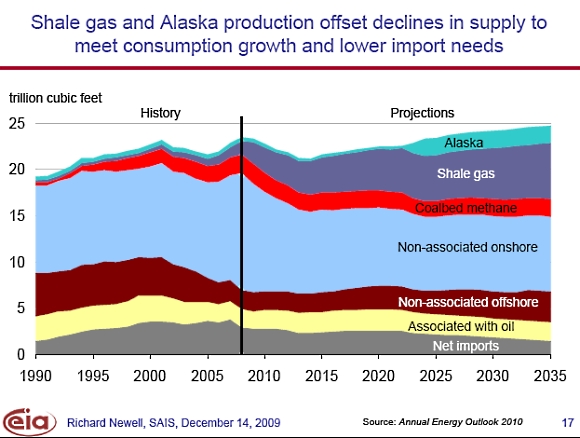

In 2009, the Energy Information Administration (part of the US Department of Energy) predicted modest increases in shale gas production (and modest decreases in conventional gas). See the chart below. Once fracking got underway, in the Obama Biden administration, conventional gas dropped further than expected, while fracking increased faster than predicted.

Trump's role as President served the energy industry well, partly by trying to reduce or eliminate regulatory obstacles to faster extraction, but perhaps more important, as a distracting show to direct outrage upon (for liberals) or something to defend (for conservatives). Meanwhile, the powers that be continued to provide bread and circuses, cheap energy and tawdry entertainment, the non-negotiable American Way of Life (AWOL).

On Inauguration Day, January 20, 2017, I was on the Global Research News Hour, a Canadian radio show and podcast, discussing how the peaking of fracking could impact the Trump administration's popularity. Since then, fracking flow rates increased substantially and peak frack will clearly be after Election Day 2020, barring some sort of violent economic shock (such as full scale war with Iran resulting in disruption of Persian Gulf oil). Whoever is in the White House when fracking subsides will likely be universally despised due to the economic tsunami this will cause. Accelerating the rate of fracking brought about a temporary illusion of continued growth but the faster any resource is extracted the shorter the time until it the flow declines or ends.

Fracking. Damned if we do, due to toxic pollution and climate chaos. Damned if we don't, because oil powers transportation of food, gas is a backbone of the electric grid and heats cold cities.

2018 Department of Energy graphic showing conventional natural gas decline versus increase of shale (fracked) gas. Non-associated and associated with oil are conventional wells (sometimes nat. gas is comingled with petroleum, sometimes it is not - it depends on how much the material was heated over the eons).

Fracking Our Future

Hydraulic fracturing -- "fracking" -- permanently pollutes groundwater, causes earthquakes and is ultrahazardous for nearby communities. The motive for fracking is not profiteering (many fracked wells lose money) but to replace declining flows of conventional oil and gas due to depletion.

Fracking provided a "stay of execution" for Peak Energy in America. It postponed energy rationing, which we are totally unprepared for, logistically and psychologically.

The economic shocks of oil rationing after fracking could trigger the biggest onslaught of scapegoating in US history, worse than the oil embargo of 1973-1974, especially since this may be permanent. How will "stop drilling" groups counter this blaming? Will there be widespread efforts to relocalize food, cooperatives established to insulate homes, share cars, repair bicycles, revitalize community interdependence? Practicalities could be much more important than protests.

The toxic impacts of hydraulic fracturing for oil and gas have been subject to public debates, protests, lawsuits, among other tactics to stop these dangers. But the other half of the fracking story, which has had much less attention, is the exaggeration of recoverable reserves.

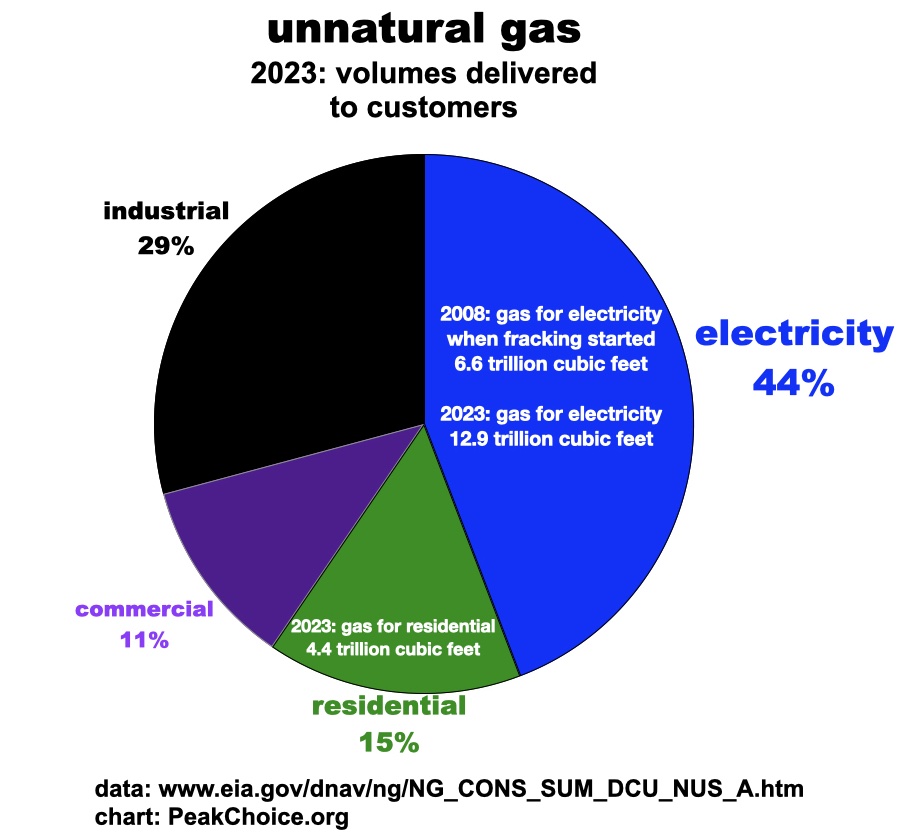

The fracking industry claims shale gas will fuel 100 years worth of USA consumption of “natural” gas. Massive drillingincreased gas production far above the 1973 natural gas peak. Gas increased its share of electric power grids, lowered coal combustion and helped scuttle plans for new nuclear reactors.

One of fracking’s dirty secrets is fracked wells decline far faster than conventional wells. Fracking a well also requires more money, technical talent and resources than conventional wells.

Fracking for oil reversed the decline of USA oil extraction since the 1970 conventional oil peak, bringing levels above that as Trump became President - and perhaps a reason why the corporatocracy tolerates Trump.

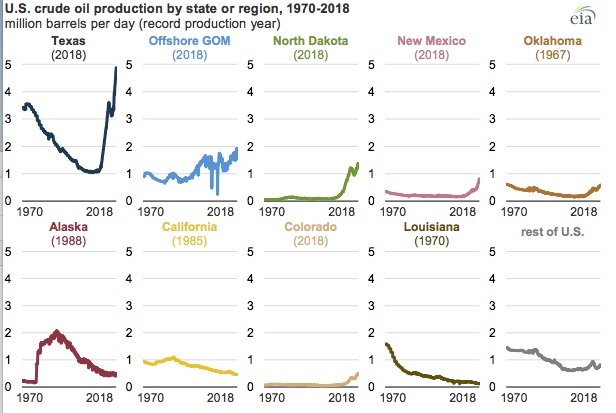

Texas oil production peaked in 1972 -- why huge efforts have been made for offshore drilling in the Gulf of Mexico, and now, via fracking. Offshore oil in the Gulf continues to move into deeper and deeper water, as the shallower spots decline. Now, the end game for fracked oil is the Permian basin in west Texas and New Mexico.

This region is slated to be the national energy sacrifice zone. National nuclear dumps are planned on the Texas - New Mexico border. The US's new uranium enrichment factory was built there, along with a "low level" nuclear dump. If the high level dump is built to receive the worst waste from the nation's power reactors, extremely lethal cargo will travel via truck, train and barge through cities across the country, risking "Mobile Chernobyl."

The Bakken shale in North Dakota has fueled wild claims of alleged energy independence and even proposals to export oil to Asia. However, Bakken has not even offset the decline of the Alaska Pipeline, which has dropped three fourths from its 1988 peak and is approaching “low flow” shutdown.

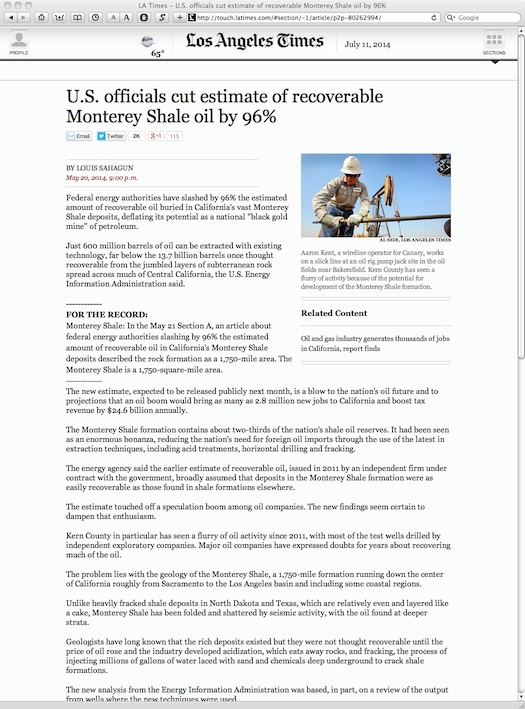

Post Carbon Institute has published reports documenting how fracking estimates have been exaggerated. They were vindicated when the Department of Energy admitted plans for oil fracking in the Monterey Shale in California had been exaggerated and downsized the estimated resource by ninety-six percent (96%). Post Carbon’s montereyoil.org website has details.

We are in a paradox at this time of Peak Everything and Climate Chaos. If we keep burning fossil fuels we will continue to wreck the biosphere, but if we suddenly stopped that would wreck civilization, which could accelerate ecological destruction (how many forests would be burned for electricity, for example). Fossil fuels allowed our population to zoom from under a billion to over seven billion today.

Fracking, deep water drilling in the Gulf of Mexico and tar sands extraction in Canada postponed gasoline rationing. We are in the eye of the energy crisis hurricane, perhaps for a few more years.

The Limits to Growth study in 1972 predicted peak resources around the turn of the century, followed by peak pollution as dirtier resources were used as higher quality resources were depleted. Fracking, tar sands, mountaintop removal and other desperate destructions seek to maintain the exponential growth economy now that the easier to extract fossil fuels are in decline.

Using solar energy since 1990 taught me that renewable energy could only run a smaller, steady state economy. Our exponential growth economy requires ever increasing consumption of concentrated resources (fossil fuels are more energy dense than renewables). A solar energy society would require moving beyond growth-and-debt based money.

After fossil fuel we will only have solar power, but that won't replace what we use now. We need to abandon the myth of endless growth on a round, and therefore, finite planet to have a planet on which to live.

Humanity does not face the question of whether to use less fossil fuels to reduce greenhouse gases, since we have reached the limits to energy growth due to geological factors. How we use the remaining fossil fuels as they deplete determines how future generations will live after the fossil fuels are gone. Will we use the second half of the fossil fuels for bigger highways or better trains? Relocalization of food production or more globalization? Resource wars or global cooperation?

"We have a supply of natural gas that can last America nearly 100 years, and my administration will take every possible action to safely develop this energy."

President Barack Obama, echoing industry exaggerations of how much frackable fuels exist

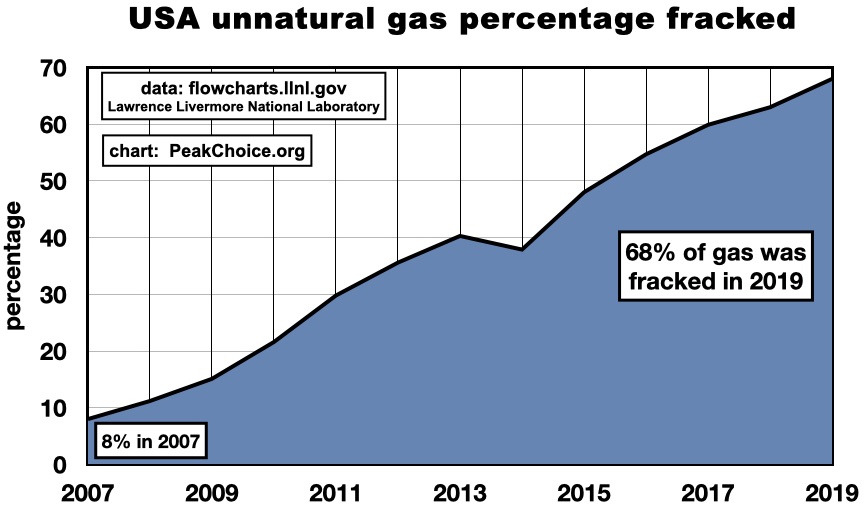

In 2013, fracked shale gas surpassed conventional natural gas wells in the USA

www.eia.gov/dnav/ng/ng_prod_sum_dcu_NUS_a.htm

https://www.eia.gov/totalenergy/data/monthly/pdf/flow/natural_gas.pdf

Fracked Oil

https://www.eia.gov/todayinenergy/detail.php?id=38992

https://www.eia.gov/todayinenergy/images/2019.04.09/chart2.svg

https://www.eia.gov/energyexplained/oil-and-petroleum-products/images/u.s.tight_oil_production.jpg

Eagle Ford, south Texas

Permian Basin, west Texas

Bakken, North Dakota and Montana

Colorado

Oklahoma

Wyoming

Monterey Shale in California

details about Monterey Shale and the illusion of 15 billion barrels at Post Carbon Institute's montereyoil.org website